One of the most common questions we hear from clients today is: “Will Social Security run out during my lifetime?”.

Whether you’re nearing retirement or still years away from claiming benefits, the answer is important and so is the plan you build around it.

- The Year 2033, Why It Matters:

- 2033 is the projected year when the Social Security trust fund reserves may run out. After that, unless changes are made, only about 79% of scheduled benefits will be payable (source: Social Security Administration).

- That’s effectively a 21% reduction in income for millions of retirees.

- If you’re counting on Social Security to help support your lifestyle in retirement, it’s crucial to start thinking about how to prepare for a potential gap in benefits.

- Key Stats and Trends to Know:

- A $40 Billion Shortfall – In 2023, Social Security expenses totaled $1.39 trillion, while revenues were only $1.35 trillion—resulting in a $40 billion gap. Most of that revenue (90%+) comes from payroll taxes and that $40 billion shortfall is expected grow as the worker to retiree ratio is shrinking (source: Social Security Administration).

- The Worker-to-Retiree Ratio Is Shrinking – Today, there are roughly 3 workers for every Social Security recipient, down from 4:1 in 1960. Projections show it could drop to 2:1 over the next 75 years (source: Pew Research Center).

- It Affects Nearly Everyone – Over 71 million Americans received benefits in 2023—about 1 in 5 U.S. residents (source: Social Security Administration).

- Legislative Proposals, A Partial Fix – A recent House tax proposal aims to ease some of the financial burden for retirees. Including, a $4,000 Federal income tax deduction for taxpayers age 65+, regardless of whether you itemize or take the standard deduction. However, this proposal does not address the core solvency issue of Social Security (source: Barron’s).

- What Might Change in the Future – To shore up the program, policymakers are exploring options such as increasing the payroll tax (currently 12.4% split between employer and employee; paid completely by self-employed individuals) or raising the full retirement age which is age 67 for those born in 1960 or later (source: Congressional Budget Office). These changes would impact both workers and retirees, making it more important to plan ahead.

- What You Can Do Today:

- Assess Risks – Evaluate how dependent your retirement plan is on Social Security and the potential implications for your long-term cash flow projections.

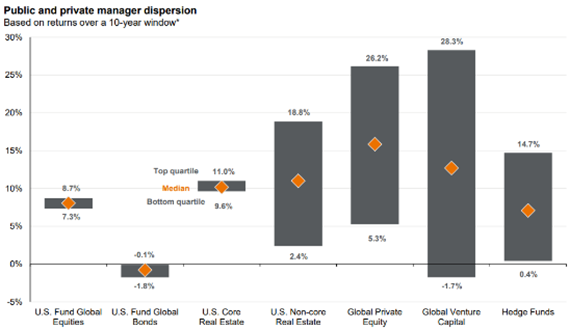

- Identify Opportunities – Build additional income streams (such as portfolio strategies focused on income-generating assets including municipal bonds or private credit) and evaluating when to take available pension or Social Security income benefits. Also, gameplan for strategies that can minimize income tax burdens in the near-term (such as tax loss selling) and for the long-term (such as Roth IRA conversions – you pay the income tax now on the conversion while future distributions can be income tax-free for your personal lifestyle spending needs or for your heirs).

Even a small shift in strategy today can help reduce reliance on uncertain benefits tomorrow. We believe that everyone’s situation is unique. Whether you’re several years from retirement or just starting to plan, we’re here to help you navigate for what’s on the horizon. If you’d like to talk through what this means for your plan, or brainstorm strategies to protect your income, please reach out to our wealth advisory team.

Waldron Private Wealth (“Company”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Pennsylvania. Company may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. For information about the Firm’s registration status and business operations, please consult Waldron’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov.

This material is for informational purposes only and is not intended to be an offer, recommendation or solicitation to purchase or sell any security or product or to employ a specific investment strategy. Due to various factors, including changing market conditions, aforementioned information may no longer be reflective of current position(s) and/or recommendation(s). Moreover, no client or prospective client should assume that any such discussion serves as the receipt of, or a substitute for, personalized advice from Company, or from any other investment professional. Investing involves risk, including the potential loss of money invested. Past performance does not guarantee future results. Asset allocation and diversification do not guarantee a profit or protect against loss. Company is neither an attorney nor an accountant, and no portion of the web site content should be interpreted as legal, accounting or tax advice.